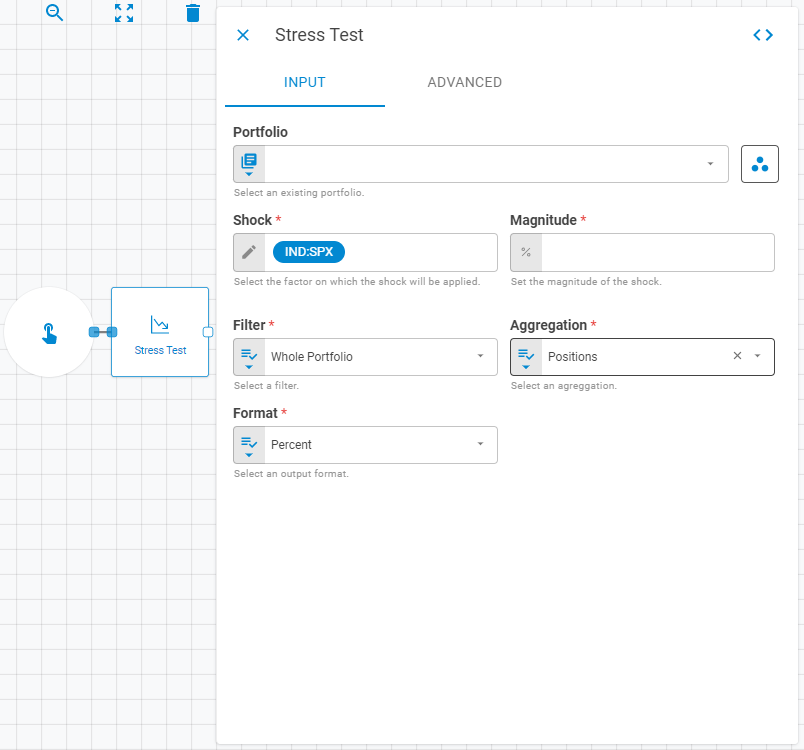

Stress Test Worker¶

The Stress Test worker calculates the expected behavior of the portfolio under different scenarios, including extreme events. It calculates the probabilities of extreme events happening and factors those probabilities into the calculations. For example: it takes into account that correlations and volatility tend to increase in periods of market distress, resulting in large price oscillations for securities.

Parameters¶

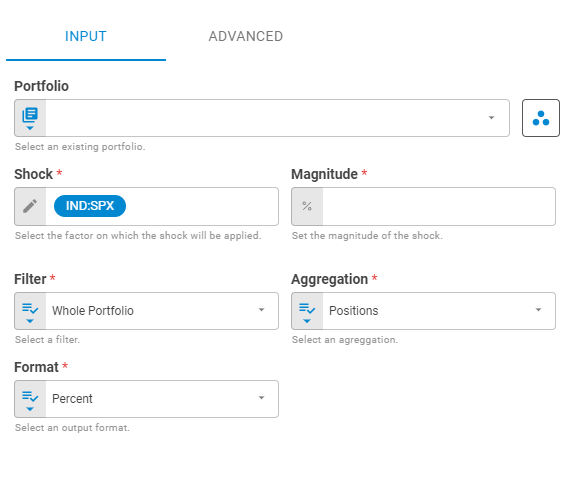

The Stress Test worker must receive specific parameters in order to execute properly. When parameters are not set correctly it may cause the worker to not work as expected. This worker's parameters are separated in the following tabs: Input and Advanced.

Input¶

The Input tab contains parameters which are consumed by the worker, in order to execute its calculations or actions.

Portfolio¶

Select the portfolio to be calculated using Fixed Portfolio, Get Latest, Get List or Upstream Data variants.

Workspace¶

Set the research workspace of the portfolio to be calculated using Fixed Workspace variant

Shock¶

Select the factor in which the shock will be applied using Select Symbol variant.

Magnitude¶

Set the magnitude of the shock using Percent variant.

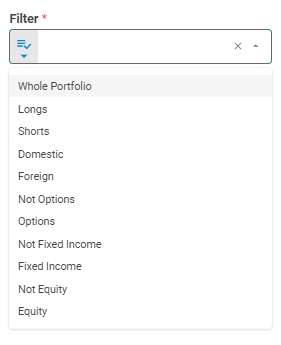

Filter¶

Select the filter to be applied in the calculation using Select variant.

Aggregation¶

Select the aggregation to be applied in the calculation using Select variant.

Time Period¶

Select the time period to be applied in the calculation using Select variant.

Format¶

Select the format in which the calculation will be performed using Select variant.

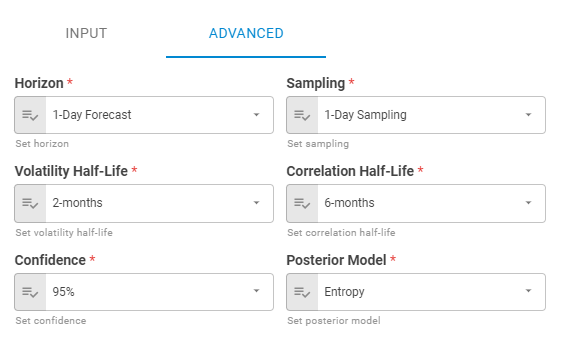

Advanced¶

The Advanced tab contains parameters that defines the worker execution results, and how it will be provided to downstream workers.

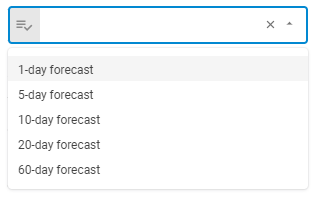

Horizon¶

Set horizon using Select variant. You can check the Sampling Combination section, on the Everysk API documentation, to know more about combinations between Horizon and Sampling.

Sampling¶

Set the sampling using Select variant. You can check the Sampling Combination section, on the Everysk API documentation, to know more about combinations between Horizon and Sampling.

Volatility Half-Life¶

Set the Volatility Half-Life using Select variant.

Correlation Half-Life¶

Set the Correlation Half-Life using Select variant.

Confidence¶

Set the Confidence using Select variant.

Posterior Model¶

Set the Posterior Model using Select variant.

Result¶

Once the worker finishes its executions successfully, it will return a result object containing the merged portfolio to the workflow, which can be used by downstream workers. Below you can see an example of the Stress Test's result object hierarchy.

- Portfolio Level (object)

- EV (number)

- Positive CVaR (number)

- Negative CVaR (number)

- Beta (number)

- Aggregation Level (object)

- Aggregation ID (string)

- EV (number)

- Positive CVaR (number)

- Negative CVaR (number)

- Info (object)

- Implied Magnitude (number)

- Implied Horizon (number)